Godrej Soaps

Godrej Soaps Ltd was a spin-off value play. It owned various popular brands, in addition to a contract manufacturing (CM) operation using their plant’s surplus capacity. Typically, the FMCG (Fast Moving Consumer Good) soap and cosmetic line of business is a lucrative one if the brand building has already been done. It was so in Godrej’s case (Godrej da jawaab nahin was a slogan I remembered from my early school days). Their marketing machinery was pretty good, worthy of giving a run for the money for the MNC brands. Cosmetic marketing is basically a combination of peer pressure and a scare tactic. It usually plays on the fear of being left out, whether it be Listerine initially in US on halitosis or Fair & Lovely cream with its play on not being fair being a marriage breaker.

However, the problem with Godrej was that it was hard to delineate the profitability of the FMCG business with the CM operation. CM operations tend to usually suck cash due to huge inventory needed. This is not true for FMCG business, where the cost of the inventory tends to be lower in relation to sales (the good ones have negative working capital). It is for a similar reason that conglomerates command a lower P/E than focused companies. The good thing with GSL was that the management was aware of this and decided on the spin-off. This made GSL a typical event play.

The spin-off of GSL into Godrej Industries Ltd (GIL) and Godrej Consumer Products Ltd (GCPL) happened and the release in value was almost immediate. I bought the whole entity at Rs.55. When GCPL listed, it started quoting at Rs.58 in Oct, 2001. The price at which GIL was quoting was all profit for me. However, attracted to the value of the intangibles, I was buying demerged GCPL in 2001. I ended up selling GIL for Rs.16 in Apr 02 and most of GCPL around 150 in Oct 03 attempting to release my capital.

I have tried to evaluate these two batches of GCPL differently. One being the spin-off play for my GSL purchases and the other a regular value play for GCPL stand-alone purchases. It turns out that the Spin-off play (GCPL, GIL collectively) returned me an IRR of 75% (monthly 4.8%) in a time period of less than 3 years. Excess return measured by NPV was at Rs.2,277 against my initial cost of 1,379 and future date NPV till 2004 was 3,199 at 12%. I sold the rest of GCPL(stand alone) in Feb 04 at around 182. It returned me 81.79% in 3 years with 5.11% monthly and NPV of 4,410.

However, I was in for another surprise with GCPL. I did not seem to have valued GCPL correctly when I sold it. In the 11 months, it went all the way up to 276. I have again and again sold early as my later evaluations will illustrate. It is very difficult for me to predict where value discovery process by the market stops and speculative activity begins. Hence, I take the best course of action that protects capital. I re-deploy it into other investments with better chances of success. In GCPL’s case I decided to buy again in Jan 05 at 277 and the returns till date have been stellar. An IRR of 123% in 15 months at a monthly rate of close to 7%. An NPV of 7,306!!!! However, this story has not ended yet.

The funny thing is I don’t seem to have evaluated the financials of GCPL. I need to do that to make sure I do not need to act soon at least to release my capital at current prices. The FMCG play in India seems pretty straight forward so far. The IT industry brought higher disposable income in the hands of the educated middle class. This is one of the aspects of growth in the services industry in a heavily populated country. A manufacturing led growth does not necessarily lead to growth in PDI. The value add (Price less material cost) for services is very high, especially so for IT industry. ( I am reminded of the infinite wisdom of the KGST who decided to tax the software CDs at their sale price. Either they had no concept of IP and intangibles or they didn’t care to make the difference).

Custom Search

Tuesday, August 22, 2006

The Plunge - 2

Reliance Industries Ltd

Reliance was almost a no-brainer. This company never posted a degrowth in turnover for the past few years. The EPS for FYE 2000 was Rs.22.82 which meant that I was getting one of the leading companies in India at around 13 P/E. However, my basis for buying was based on the assumption that the EPS of RIL will grow at 25% going forward and I would be able to sell it at the same P/E some years forward. 25% seemed realistic looking at the growth from 1999 to 2000. In retrospect, I made two errors due to plain ignorance.

Over the period of 4 years following, I seem to have gotten back my entire capital back through some sales (it is a strategy I follow) and still hold the same value of RIL. As on 3/31/06, it roughly translates to an annualised return of 34.5% at a monthly rate of 2.5%.

Measuring Performance

The returns I will be using here are monthly rupee weighted returns linked geometrically to produce the annual return. There are two prominent and valid methods of measuring return. One is to measure the growth of a unit of currency over a period of time and the other is to measure the return weighted for the transactions for each period. The first measure is more appropriate when calculating returns for something where the entity being measured does not have control over the cashflows. Money-weighted returns (basic as an IRR) is more appropriate where the entity measured has control over cashflows. Clearly, this method is appropriate for my purposes, since I am in charge of sale/purchase decisions and investment of cashflows.

IRR has an inherent flaw in that it assumes the cashflows are invested at the same rate throughout the period of investment. However, that may not be necessarily the case here. I may have reinvested the money in other investments which may have yielded more or less than RIL. However, the difference in measurement will vary dependant on the scale of the investment in relation to the total portfolio, the range difference in returns between the various investments in the portfolio and their interaction.

Another method, I used to measure the returns was NPV. Net Present Value is the incremental value after investing at your required return. So an NPV of 0 means that your investment returned exactly the same as your required return. Anything more would be the incremental return discounted to the initial period of investment at the required rate of return. Now, we run into the question as to what is the appropriate rate of required return.

If you follow the economist’s line of thinking that capital is scarce with alternative uses, the cost of capital is the return on next best available investment; the alternative for Indian stocks may be Indian fixed income instruments. I have looked at returns of 364-day T-bill rates. However, I am following the well researched view that Indian G-Secs are not priced appropriately to adjust for inflation appropriately due to a demand imbalance from PSU Banks. The alternative investment I could find was small savings. These are comparable, especially since the time-frame of the investment under review and the SS is almost the same. NSCs would be an appropriate instrument. Adjusting for the tax effects of taxability, deductibility and rebatability under tax laws; I am going to use an approximate rate of 12% as required return.

Back to RIL

Looking at RIL, I find that my NPV is 22,641 at 12%. This is the excess return discounted back to April 2001. The value as of April 2006 will be 39,902 (that is 22,641 invested at 12% for 5 years). Considering that my investment outgo has only been 40,618, this is a very good excess return.

Measuring Performance in Dollars

A side note – The US dollar return for all the investments under evaluation would be more than the stock’s return by around 1.4% per year and for 5 years ending 03/31/06 would be around 7% (from INR 47.69 to 44.60). This means that to calculate the US Dollar return (%) –

[(1 + S) (1 + E)] -1

where S is the Stock Return in % and E is the exchange rate gain/loss in %

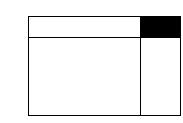

At first sight, it may seem that the US Dollar return would be as easy as adding up the US Dollar gain/loss and the stock return. However, the correct way to look at it is in terms of area of a rectangle, where the S & E are the increase in the sides of the rectangle. If the length (assume S) increases with breadth remaining constant, the area would increase proportionate to the increase in length. The same is also true for an increase in breadth. However, when both S & E change, there is a corner rectangle formed by the interaction of the two as illustrated in the following diagram. In additive method of calculating US Dollar return, this smaller rectangle formed by the interaction is left out. This corner rectangle is the result of the stock gain increasing due to increase in currency return as well.

In RIL’s case, US Dollar return would be 36.37% [(1 + .345) (1 + .014)-1]

So much for history of RIL, the question now to be considered is will RIL continue to deliver similar stellar performance in the next 5 years?

Reliance was almost a no-brainer. This company never posted a degrowth in turnover for the past few years. The EPS for FYE 2000 was Rs.22.82 which meant that I was getting one of the leading companies in India at around 13 P/E. However, my basis for buying was based on the assumption that the EPS of RIL will grow at 25% going forward and I would be able to sell it at the same P/E some years forward. 25% seemed realistic looking at the growth from 1999 to 2000. In retrospect, I made two errors due to plain ignorance.

- I assumed that the P/E ratio was reasonable considering the then prevailing interest rate environment.

- I assumed that growth would follow a linear trend.

Over the period of 4 years following, I seem to have gotten back my entire capital back through some sales (it is a strategy I follow) and still hold the same value of RIL. As on 3/31/06, it roughly translates to an annualised return of 34.5% at a monthly rate of 2.5%.

Measuring Performance

The returns I will be using here are monthly rupee weighted returns linked geometrically to produce the annual return. There are two prominent and valid methods of measuring return. One is to measure the growth of a unit of currency over a period of time and the other is to measure the return weighted for the transactions for each period. The first measure is more appropriate when calculating returns for something where the entity being measured does not have control over the cashflows. Money-weighted returns (basic as an IRR) is more appropriate where the entity measured has control over cashflows. Clearly, this method is appropriate for my purposes, since I am in charge of sale/purchase decisions and investment of cashflows.

IRR has an inherent flaw in that it assumes the cashflows are invested at the same rate throughout the period of investment. However, that may not be necessarily the case here. I may have reinvested the money in other investments which may have yielded more or less than RIL. However, the difference in measurement will vary dependant on the scale of the investment in relation to the total portfolio, the range difference in returns between the various investments in the portfolio and their interaction.

Another method, I used to measure the returns was NPV. Net Present Value is the incremental value after investing at your required return. So an NPV of 0 means that your investment returned exactly the same as your required return. Anything more would be the incremental return discounted to the initial period of investment at the required rate of return. Now, we run into the question as to what is the appropriate rate of required return.

If you follow the economist’s line of thinking that capital is scarce with alternative uses, the cost of capital is the return on next best available investment; the alternative for Indian stocks may be Indian fixed income instruments. I have looked at returns of 364-day T-bill rates. However, I am following the well researched view that Indian G-Secs are not priced appropriately to adjust for inflation appropriately due to a demand imbalance from PSU Banks. The alternative investment I could find was small savings. These are comparable, especially since the time-frame of the investment under review and the SS is almost the same. NSCs would be an appropriate instrument. Adjusting for the tax effects of taxability, deductibility and rebatability under tax laws; I am going to use an approximate rate of 12% as required return.

Back to RIL

Looking at RIL, I find that my NPV is 22,641 at 12%. This is the excess return discounted back to April 2001. The value as of April 2006 will be 39,902 (that is 22,641 invested at 12% for 5 years). Considering that my investment outgo has only been 40,618, this is a very good excess return.

Measuring Performance in Dollars

A side note – The US dollar return for all the investments under evaluation would be more than the stock’s return by around 1.4% per year and for 5 years ending 03/31/06 would be around 7% (from INR 47.69 to 44.60). This means that to calculate the US Dollar return (%) –

[(1 + S) (1 + E)] -1

where S is the Stock Return in % and E is the exchange rate gain/loss in %

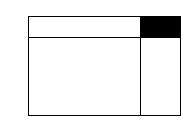

At first sight, it may seem that the US Dollar return would be as easy as adding up the US Dollar gain/loss and the stock return. However, the correct way to look at it is in terms of area of a rectangle, where the S & E are the increase in the sides of the rectangle. If the length (assume S) increases with breadth remaining constant, the area would increase proportionate to the increase in length. The same is also true for an increase in breadth. However, when both S & E change, there is a corner rectangle formed by the interaction of the two as illustrated in the following diagram. In additive method of calculating US Dollar return, this smaller rectangle formed by the interaction is left out. This corner rectangle is the result of the stock gain increasing due to increase in currency return as well.

In RIL’s case, US Dollar return would be 36.37% [(1 + .345) (1 + .014)-1]

So much for history of RIL, the question now to be considered is will RIL continue to deliver similar stellar performance in the next 5 years?

The Plunge - 1

By then a lot had happened. The bull market of 2000 had crashed. There were a lot of buying opportunities. Mr.Market had hung a sign outside ‘Dalal Street’ with a huge “On Sale” sign. The day I bought my first shares, a stockbroker in Delhi committed suicide along with his family, because he couldn’t pay his debts. Not to lighten the tragedy of unnecessary waste of human life, the coincidence was too striking to me – reaffirming that I was definitely on the right path. My first purchase were two scrips:-

Reliance Industries Ltd (http://www.ril.com/) - 10 shares at Rs.300 – Rs.3,007.50

Godrej Soaps Ltd – 25 shares at Rs.55 – Rs.1,378.50.

Reliance Industries Ltd (http://www.ril.com/) - 10 shares at Rs.300 – Rs.3,007.50

Godrej Soaps Ltd – 25 shares at Rs.55 – Rs.1,378.50.

Sunday, August 20, 2006

Testing the Waters

Testing the Waters – Waiting for Demat

My initial experience in buying stocks in the secondary markets had been a disaster. Circa 1996 (I wasn’t even 20 then), I audited a stockbroker for my employer and established a business relationship with them. I scoured through ET stock pages and bought two stocks. My criterion was that they were trading near their 52-week lows. (Behavioral Finance calls it Reference Point behavior). Of course, I didn’t bother to check if there was any valid reason for such a price behavior. Here are the purchase prices:-

GR Magnets Ltd – 100 shares at Rs.8.72 per share

Goodearth Organics Ltd – 100 shares at Rs.1.00 (approximately) per share

I don’t exactly recall the price I paid for Goodearth. I just know that I paid less than a 1000 to the broker in settlement.

When I placed the order, the lady at the broker’s asks me – did I know that GR Magnets’ Managing Director was arrested for FERA violations (foreign exchange laws)? Of course, I had no idea. But, I nodded along.

Electronic trading and demat were unheard of these days. The broker delivered to me a share certificate with attached transfer deed, where the seller had signed his name and with a few other prior parties’ signatures. I had no idea of the timing of the sale. So, when asked I said I wanted it transferred to my name. (It didn’t occur to me to ask for alternatives – I could have held on to the transfer deed and get it revalidated after three months, if I didn’t sell it by then. Three months, I think, was the time limit to hold the deed without sending it to the company). So I filled out the forms and send it on its merry way to the companies to get the shares transferred.

Here’s the rest of the story:-

GR Magnets – bounced up to Rs.20 within 2-3 months. Good call, I thought. However, there was one hitch. I didn’t have the shares with me to sell it. It was with the company to be transferred. By the time I got the shares back, the scrip was moved to the Z list (equivalent of having the bad boys of the class sit in the backbenches) and was trading way below my purchase price. The last quoted price was close to Rs.1. I still have this certificate and am thinking of framing it as a not-so gentle reminder of my follies of indiscretion.

Goodearth Organics – never saw a bounce, never saw the certificate again.

It was a great practical lesson in bad deliveries for me. I stayed away from the markets for the next five years, until demat came into existence.

My initial experience in buying stocks in the secondary markets had been a disaster. Circa 1996 (I wasn’t even 20 then), I audited a stockbroker for my employer and established a business relationship with them. I scoured through ET stock pages and bought two stocks. My criterion was that they were trading near their 52-week lows. (Behavioral Finance calls it Reference Point behavior). Of course, I didn’t bother to check if there was any valid reason for such a price behavior. Here are the purchase prices:-

GR Magnets Ltd – 100 shares at Rs.8.72 per share

Goodearth Organics Ltd – 100 shares at Rs.1.00 (approximately) per share

I don’t exactly recall the price I paid for Goodearth. I just know that I paid less than a 1000 to the broker in settlement.

When I placed the order, the lady at the broker’s asks me – did I know that GR Magnets’ Managing Director was arrested for FERA violations (foreign exchange laws)? Of course, I had no idea. But, I nodded along.

Electronic trading and demat were unheard of these days. The broker delivered to me a share certificate with attached transfer deed, where the seller had signed his name and with a few other prior parties’ signatures. I had no idea of the timing of the sale. So, when asked I said I wanted it transferred to my name. (It didn’t occur to me to ask for alternatives – I could have held on to the transfer deed and get it revalidated after three months, if I didn’t sell it by then. Three months, I think, was the time limit to hold the deed without sending it to the company). So I filled out the forms and send it on its merry way to the companies to get the shares transferred.

Here’s the rest of the story:-

GR Magnets – bounced up to Rs.20 within 2-3 months. Good call, I thought. However, there was one hitch. I didn’t have the shares with me to sell it. It was with the company to be transferred. By the time I got the shares back, the scrip was moved to the Z list (equivalent of having the bad boys of the class sit in the backbenches) and was trading way below my purchase price. The last quoted price was close to Rs.1. I still have this certificate and am thinking of framing it as a not-so gentle reminder of my follies of indiscretion.

Goodearth Organics – never saw a bounce, never saw the certificate again.

It was a great practical lesson in bad deliveries for me. I stayed away from the markets for the next five years, until demat came into existence.

Subscribe to:

Posts (Atom)