Reliance was almost a no-brainer. This company never posted a degrowth in turnover for the past few years. The EPS for FYE 2000 was Rs.22.82 which meant that I was getting one of the leading companies in India at around 13 P/E. However, my basis for buying was based on the assumption that the EPS of RIL will grow at 25% going forward and I would be able to sell it at the same P/E some years forward. 25% seemed realistic looking at the growth from 1999 to 2000. In retrospect, I made two errors due to plain ignorance.

- I assumed that the P/E ratio was reasonable considering the then prevailing interest rate environment.

- I assumed that growth would follow a linear trend.

Over the period of 4 years following, I seem to have gotten back my entire capital back through some sales (it is a strategy I follow) and still hold the same value of RIL. As on 3/31/06, it roughly translates to an annualised return of 34.5% at a monthly rate of 2.5%.

Measuring Performance

The returns I will be using here are monthly rupee weighted returns linked geometrically to produce the annual return. There are two prominent and valid methods of measuring return. One is to measure the growth of a unit of currency over a period of time and the other is to measure the return weighted for the transactions for each period. The first measure is more appropriate when calculating returns for something where the entity being measured does not have control over the cashflows. Money-weighted returns (basic as an IRR) is more appropriate where the entity measured has control over cashflows. Clearly, this method is appropriate for my purposes, since I am in charge of sale/purchase decisions and investment of cashflows.

IRR has an inherent flaw in that it assumes the cashflows are invested at the same rate throughout the period of investment. However, that may not be necessarily the case here. I may have reinvested the money in other investments which may have yielded more or less than RIL. However, the difference in measurement will vary dependant on the scale of the investment in relation to the total portfolio, the range difference in returns between the various investments in the portfolio and their interaction.

Another method, I used to measure the returns was NPV. Net Present Value is the incremental value after investing at your required return. So an NPV of 0 means that your investment returned exactly the same as your required return. Anything more would be the incremental return discounted to the initial period of investment at the required rate of return. Now, we run into the question as to what is the appropriate rate of required return.

If you follow the economist’s line of thinking that capital is scarce with alternative uses, the cost of capital is the return on next best available investment; the alternative for Indian stocks may be Indian fixed income instruments. I have looked at returns of 364-day T-bill rates. However, I am following the well researched view that Indian G-Secs are not priced appropriately to adjust for inflation appropriately due to a demand imbalance from PSU Banks. The alternative investment I could find was small savings. These are comparable, especially since the time-frame of the investment under review and the SS is almost the same. NSCs would be an appropriate instrument. Adjusting for the tax effects of taxability, deductibility and rebatability under tax laws; I am going to use an approximate rate of 12% as required return.

Back to RIL

Looking at RIL, I find that my NPV is 22,641 at 12%. This is the excess return discounted back to April 2001. The value as of April 2006 will be 39,902 (that is 22,641 invested at 12% for 5 years). Considering that my investment outgo has only been 40,618, this is a very good excess return.

Measuring Performance in Dollars

A side note – The US dollar return for all the investments under evaluation would be more than the stock’s return by around 1.4% per year and for 5 years ending 03/31/06 would be around 7% (from INR 47.69 to 44.60). This means that to calculate the US Dollar return (%) –

[(1 + S) (1 + E)] -1

where S is the Stock Return in % and E is the exchange rate gain/loss in %

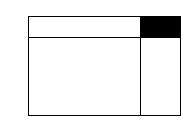

At first sight, it may seem that the US Dollar return would be as easy as adding up the US Dollar gain/loss and the stock return. However, the correct way to look at it is in terms of area of a rectangle, where the S & E are the increase in the sides of the rectangle. If the length (assume S) increases with breadth remaining constant, the area would increase proportionate to the increase in length. The same is also true for an increase in breadth. However, when both S & E change, there is a corner rectangle formed by the interaction of the two as illustrated in the following diagram. In additive method of calculating US Dollar return, this smaller rectangle formed by the interaction is left out. This corner rectangle is the result of the stock gain increasing due to increase in currency return as well.

In RIL’s case, US Dollar return would be 36.37% [(1 + .345) (1 + .014)-1]

So much for history of RIL, the question now to be considered is will RIL continue to deliver similar stellar performance in the next 5 years?

No comments:

Post a Comment